Information correct as of June 2026

Claim reimbursement for customs duty paid or reclaim state aid used on ‘at risk’ goods brought into Northern Ireland (NI), if you can show they were sold or used outside the European Union (EU).

As a result of the Windsor Framework, HM Government (HMG) launched the Duty Reimbursement Scheme (DRS) on 30 June 2023. Traders can reclaim EU customs duty paid or the state aid used – also known as ‘replenishment of state aid’ – on goods that moved to NI which did not subsequently move into the EU. For further details, see the Apply to claim a repayment or remission of import duty, or reclaim state aid used on ‘at risk’ goods brought into Northern Ireland guidance on GOV.UK.

The scheme enables the repayment of duties or the state aid used, where the necessary evidence is provided and is backdated, to provide reimbursement for relevant duties for goods moved from 1 January 2021.

Important: The deadline for backdated claims covering duty paid between 1 January 2021 and 30 June 2023 is approaching: these claims must be submitted by 30 June 2026.

For the claim to be successful, traders are required to provide evidence that goods were sold or used in NI, moved elsewhere within the United Kingdom (UK), or exported outside the UK or EU.

Frequently asked questions

What is the Duty Reimbursement Scheme (DRS)?

The DRS allows traders to reclaim EU duties paid or the state aid used on goods that have moved to NI and been declared ‘at risk’, providing traders can supply evidence to show the goods did not enter the EU.

How can the TSS support me?

Your Trader Support Service (TSS) declaration contains information that is required for the claim, such as:

- The Movement Reference Number (MRN)

- Your GB or XI EORI number

- The amount of import duty that was paid to HM Revenue & Customs (HMRC)

This information is available on a completed Supplementary Declaration or a Full Frontier Declaration.

The TSS Contact Centre can support you to obtain this information. The contact number is 0800 060 8888. If you are not registered with the TSS, visit our Registering Your Business page.

How do I get the information from the TSS Portal to make a claim?

You can export a copy of your declaration from the TSS Portal. This is required as evidence for your claim. You can do this by following the instructions in section 8.3 (‘Produce a Report of Declarations with Duty Paid’) of the How to use the TSS Portal guide on NICTA.

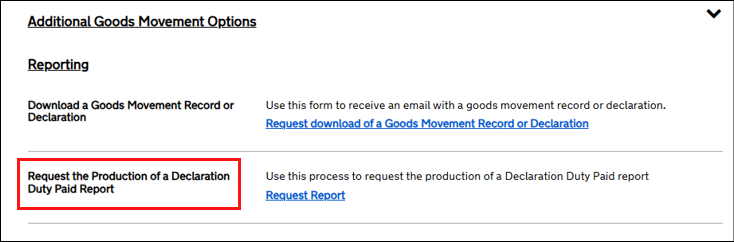

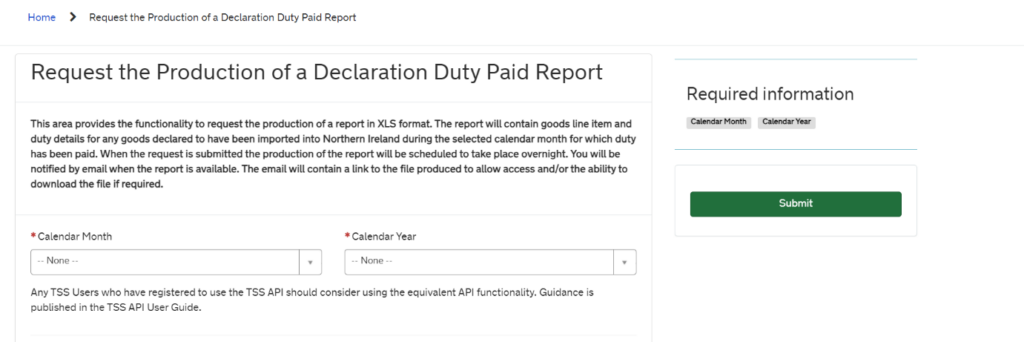

Is there a report function I can use for multiple declarations in the TSS Portal?

Yes, there is a report available in TSS for all declarations by line items with duty paid within a calendar month.

Traders should navigate to Start a Goods Movement from the TSS Portal home page and select the option to Request the Production of a Declaration Duty Paid Report. This appears between the existing ‘Export a Declaration’ and ‘Inventory Linking’ options:

The report will contain details of all Supplementary Declarations within the specified calendar month, in which goods line items contain paid duty. The report will be created as an Excel spreadsheet.

When a request for a ‘Declaration Duty Paid Report’ is completed successfully within the TSS platform, an email will be sent to the trader to advise them that the report is now available and can be accessed from the hyperlink provided in the email.

What is the main criteria reasons for a reimbursement claim?

There are scenarios where a trader may claim a reimbursement for goods brought to NI, where the goods:

- Remain in NI

- Move onwards to Great Britain (GB: England, Scotland and Wales)

- Are exported to a country outside the UK and the EU

What does ‘at risk’ mean?

Goods are ‘at risk’ if they enter NI but may later be sold or consumed in the EU and are therefore subject to EU tariffs.

See NICTA guidance on ‘Tariffs on goods movements into NI’.

When can I claim?

You can submit claims for goods movements dating back to 1 January 2021.

You will need to claim:

- By 30 June 2026, if you have paid duty between 1 January 2021 and 30 June 2023

- Within 3 years following notification of the duty, if you were notified after 30 June 2023

If you are reclaiming state aid used to waive duty, you should claim as soon as the supporting evidence is available.

How can I make a claim?

You can make a claim using the Apply to claim a repayment or remission of import duty or reclaim state aid used on ‘at risk’ goods brought into Northern Ireland form on GOV.UK.

You will need to sign in with your Government Gateway ID and password and complete the digital form. (If you do not have a user ID, you can create one when you first try to sign in.)

What can I claim reimbursement for?

You can claim reimbursement for EU customs duty paid on ‘at risk’ goods brought to NI where you have sufficient evidence to show the goods did not enter the EU.

- For movements of goods from GB to NI, you can claim for the full amount of EU customs duty paid

- For imports to NI from a country outside the UK or EU, if the EU duty was greater than the UK duty at the time of import, you can claim for the difference between the two rates

You may be eligible to reclaim state aid used to waive import duty through the Customs Duty Waiver Scheme (CDWS) if the goods you used the waiver for then:

- Remain in NI

- Move onwards to GB (England, Scotland and Wales)

- Are exported to a country outside the UK and EU

Who can claim?

You must be the Importer of Record for the original ‘at risk’ movement to NI, or an agent or representative acting on behalf of the Importer of Record.

Can I make a claim for some of my goods on a consignment?

Yes, you can submit a claim for a portion of the import duty paid on a consignment of ‘at risk’ goods.

For example: If you move a consignment of 100 pieces of ‘at risk’ goods to NI, and 50 of those pieces subsequently meet the reimbursement conditions, then you can claim back the duty charged on those pieces.

What evidence do I need to make a claim?

This depends on the scenario under which the reimbursement claim is being made. All claims will be assessed on a case-by-case basis. A non-exhaustive list of evidence types is available in the Before you claim section on GOV.UK. Some examples include:

- Export declaration

- Sales invoice

- Commercial evidence, such as a VAT invoice

- Evidence of customer orders

- Packing list

- Transport documents

- Manifest data

- Bill of lading

- Inventory records

- Contracts for sale

If the goods you moved to NI have been processed, you will need to provide additional evidence with your reimbursement claim. This may include evidence of the inputs, processing and outputs to demonstrate that the goods you moved to NI later met one of the criteria set out above.

Additional evidence may be required if your goods are subject to EU trade defence measures, and further information is available in the Before you claim section on GOV.UK.

How would I evidence goods for retail sale or use in NI?

For example, you could submit a sales invoice or receipt showing sale of the goods to a consumer located in NI or a contract for the sale.

Note: Where goods are sold onto another business or retailer in NI, commercial records will be required, including any assurance from the business that they intend to sell the goods to a consumer in NI, such as written agreements.

Further information is available in the Before you claim section on GOV.UK.

How would I evidence goods consumed in NI?

For example, you could submit commercial documents and records showing evidence of actual consumption, such as inventory records showing that fuel has been used. Alternatively, you could provide internal records showing that a substance has been entirely consumed.

Further information is available in the Before you claim section on GOV.UK.

How would I evidence goods permanently installed in NI?

For example, you could submit commercial documents and records showing goods have been permanently installed in NI, such as a certification of the installation of goods provided by building inspectors or other appropriate authorities.

Further information is available in the Before you claim section on GOV.UK.

How would I evidence goods destroyed in NI?

For example, you could submit a commercial invoice for imported goods, inventory records and destruction certificates, such as a DVLA certificate of destruction in the case where a vehicle has been scrapped.

Further information is available in the Before you claim section on GOV.UK.

How would I evidence goods moved from NI to GB?

For example, you could submit a sales invoice or a contract for sale of the goods to a business or consumer located in GB, along with transport documents to show that the goods have been transported from NI to GB.

Further information is available in the Before you claim section on GOV.UK.

How would I evidence goods exported to Rest of World (a location outside of the UK or the EU)?

For example, you need to submit an export declaration and the MRN to show the goods have been removed from NI to a location outside the EU, as well as a sales invoice showing the final billing destination of the purchaser and shipping address for the goods as outside the EU.

Further information is available in the Before you claim section on GOV.UK.

Can I make a claim when I cannot trace imports on a one-to-one basis?

If you cannot provide direct evidence tracing your goods from import to their final destination, you may still be eligible to make a DRS claim if your goods are considered interchangeable.

Can I make a claim if my goods are considered interchangeable?

Yes, if your goods are interchangeable, you can claim a repayment for ‘at risk’ duty paid on goods, as long as you can demonstrate that equivalent goods have either remained in NI, been moved to GB or moved to a country outside the EU and UK. You must provide evidence to demonstrate that the goods qualify as interchangeable goods.

How would I evidence my goods qualify as interchangeable goods?

To qualify, the goods must all have the:

- Same 8-digit commodity code. Evidence for this could be either the customs declaration, commercial invoice or packing list showing the same commodity code

- Same commercial quality. Evidence for this could be product specifications or laboratory test reports showing the goods have the same technical standards or performance

- Ability to be swapped for each other. Evidence for this could be purchase contracts stock or substitution records confirming that the goods may be used in place of others

Further information on goods qualifying as interchangeable, including examples, is available in the Before you claim section on GOV.UK.

How many claims can I make?

There is no limit to the number of claims you can make.

Can I make more than one claim at a time?

Yes, you can submit a bulk claim to cover multiple movements of goods. You can do this as long as the claims are all based on the same reimbursement scenario, for example ‘retail sale in NI’ or ‘destruction of goods in NI’. Bulk claims containing more than one scenario will be rejected. The bulk claim must also be for the same importer.

There is a limit of 250 individual consignments or MRNs per bulk claim.

For example, you may wish to make a bulk claim in the following scenario:

- You made multiple movements of ‘at risk’ goods to NI

- The goods were all destroyed in NI

To make sure your bulk claim is accepted:

- You must submit separate claims for different payment types

- If you are reclaiming state aid, you must only include MRNs from the same month

Goods subject to an EU trade defence measure cannot be included in a bulk claim.

You do not need to supply evidence for all goods movements with your claim. Instead, you will need to hold the relevant evidence that relates to each individual movement of goods covered in a bulk claim and be able to provide this upon request from HMRC.

Can I claim for the EU duty that was passed on to me because the importer paid EU duty because the goods were at risk?

No, you must be the Importer of Record for the original ‘at risk’ movement to NI, or an agent acting on behalf of the Importer of Record.

What happens after I have submitted a claim?

You will get an email to confirm that HMRC has received the form. This email will contain a unique reference number.

You do not need to do anything further until HMRC writes to you regarding your claim. HMRC will notify you by letter if your claim is approved.

If your claim is approved HMRC:

- Will reimburse the duty by the method selected when you made your claim

- Will amend your state aid balance in your CDWS digital service account if you have reclaimed state aid

Alternatively, HMRC may ask you to provide additional evidence to support your claim.

Ready to apply?

Complete the Apply to claim a repayment or remission of import duty or reclaim state aid used on ‘at risk’ goods brought into Northern Ireland form on GOV.UK.

Still have questions?

If you need more information, contact the TSS Contact Centre.